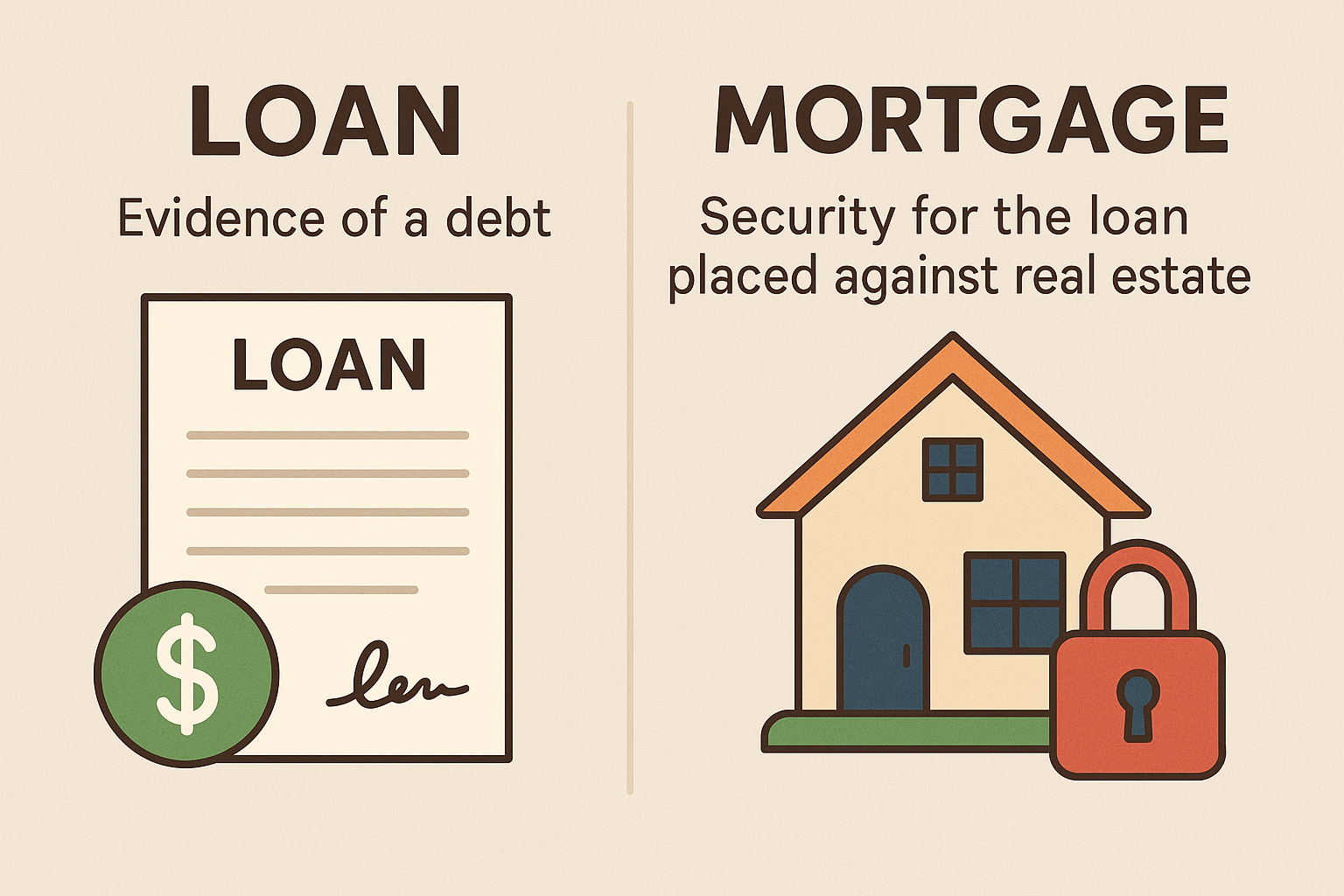

It is crucial to understand the difference between a loan and a mortgage.

- A loan is the actual financial agreement; the advance of money from a lender to a borrower under specific terms, including the principal amount, interest rate, repayment schedule and fees.

- A mortgage is the legal instrument that secures the loan. It grants the lender a security interest in a specific parcel of real estate. This legal document is registered on the title of the property through the provincial land registry system. This registration establishes the lender’s priority and legal right to the property in the event of a default. The borrower may not sell or refinance the real estate without repaying the registered creditors.

1.3 | Enforcement and Security

A mortgage secures a debt by giving the lender specific legal rights against the borrower and the property. When a mortgage is registered against title to a property, it becomes a charge on the land that “runs with” the property. This means that if a borrower tries to sell the property, the purchaser would acquire it subject to that registered mortgage unless it is discharged. In practice, buyers will not accept title with an existing mortgage (unless it is being formally “assumed”), so the borrower must pay out or refinance the mortgage before the transfer can close. Similarly, when a borrower tries to refinance with a new lender, the new lender will generally require that any prior mortgages be discharged or subordinated, since otherwise the new loan would rank behind the existing charge.

One of the primary functions of a mortgage is to establish priority in debt collection. When the mortgage is registered in the provincial land title or land registry system, it provides public notice of the lender’s interest and fixes the lender’s priority over other creditors. Generally, the principle of “first to register” applies, subject to statutory exceptions such as municipal tax liens or construction liens that may take precedence.

Beyond priority, the mortgage agreement itself sets out the borrower’s obligation to repay the principal, interest and any other amounts due. If the borrower defaults, the lender is entitled to accelerate the loan and declare the entire balance immediately payable.

The mortgage also gives the lender remedies against the land itself. Depending on the province, the lender may exercise a power of sale, apply for a judicial sale or seek foreclosure, which results in the lender taking title to the property and extinguishing the borrower’s right to redeem. In some cases, lenders may also take possession to collect rents or preserve the property, though this is less common in practice.

If the sale of the mortgaged property does not cover the outstanding debt, the lender typically has the right to pursue a deficiency judgment against the borrower personally for the shortfall. This right, however, is not absolute. Some provinces restrict or prohibit deficiency claims, particularly in cases involving certain residential mortgages.

Mortgages must be understood in relation to other security interests. Although personal property security legislation (such as the PPSA in most provinces) governs movable assets, land remains outside that regime and is instead regulated by provincial land law frameworks. This means that while lenders may hold multiple forms of security against a borrower, the mortgage retains a unique status in protecting real property collateral.

Multiple mortgages can exist on the same property, with their priority determined by registration order or contractual arrangements between creditors. In this way, mortgages not only secure repayment but also shape the legal hierarchy among creditors competing for the same debtor’s assets.